Traditional IRA : One of the Most Common Retirement Tools & The Hidden Trade-Offs You Should Know

Everyone knows about IRAs, but few truly understand how they work... The advantages they bring and the tax bill you're deferring into the future

Let's walk through what a traditional IRA is, how it fits into your retirement plan & what most advisors don't tell you.

So what is a Traditional IRA?

Simply put an Traditional IRA is an Individual Retirement Account that allows you to contribute money into a personal retirement account and defer taxes until you withdraw the money.

Defer = to put off

(an action or event) to a later time; postpone.

Is the amount in taxes you'll pay when you do withdraw your funds specified ??

Quick Question...?

Nope. You'll be taxed on that withdrawal at the current rate of taxation for ordinary income according to the tax brackets at the time of the withdrawal.

So while not paying any tax right now sounds amazing.. Let's dive into how it could possibly affect your retirement income.

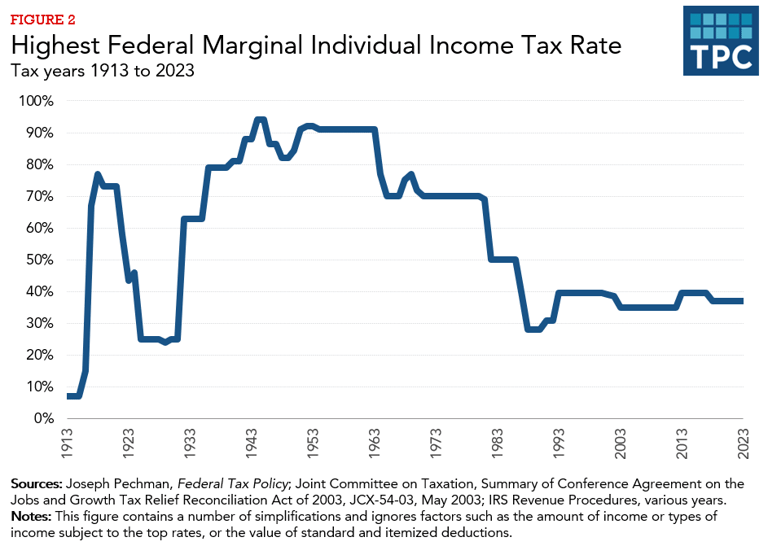

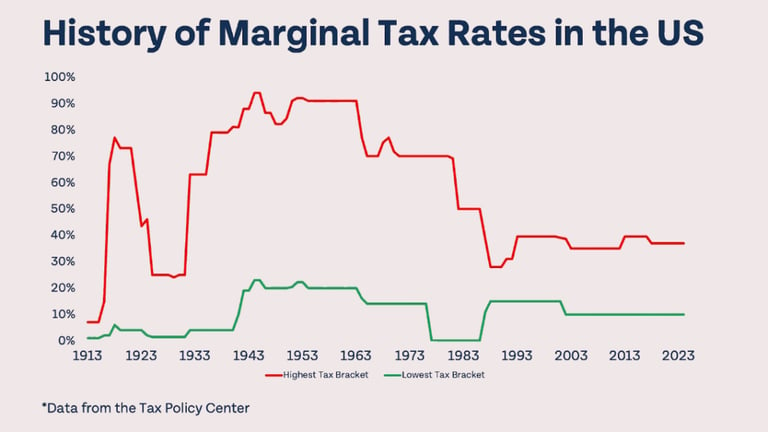

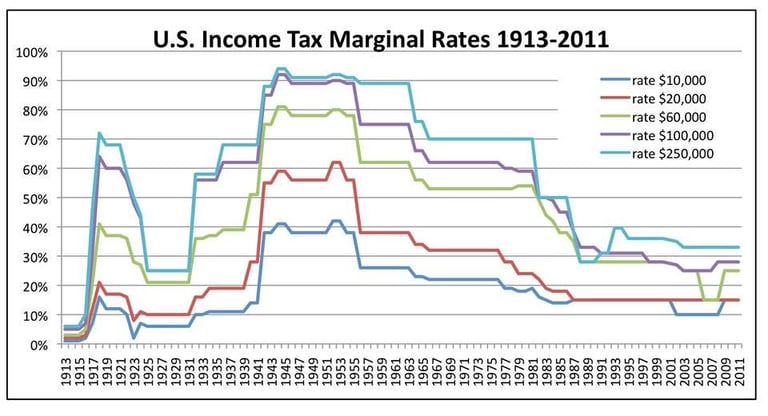

Here's some charts I'd like to take into consideration

What you can see here is the historical tax rate on income for different income levels. As you can see on the far right the trend is similar just at a lower level for the lower earner.

According to these charts we're paying average if not lower than average taxes on our income right now... With the way taxes rose so drastically in the 30s are you willing to gamble on the amount of tax you'll have to pay on your retirement income in the future ??

Just something to think about...

Let's not forget that tax isn't the only thing not guaranteed in these accounts... IRAs are tied directly to market performance so if the market tanks so does your IRA

I wonder if there's a way to not have to pay an unknown amount of taxes in the future and also be protected from market downturns when it comes to saving for my retirement....

Let's talk quick about how much you can put in these things...

For 2024 and 2025, you can contribute up to $7,000 to a traditional or Roth IRA, or $8,000 if you are age 50 or older. This total contribution limit applies to all of your IRAs (traditional and Roth combined) and cannot exceed your taxable compensation for the year, whichever is less. Roth IRA contributions may be limited based on your Modified Adjusted Gross Income (MAGI)

Wait what's a Roth ???

Click here to learn about Roths --->

Somethings not adding up... If you can only save 7k a year... Even if you max this thing out every year you could only save up 210k in 30 years in this account... That's not much to retire on

Granted you should have multiple accounts for your retirement.. All your eggs in one basket is rarely ever a good thing.

Wouldn't it be cool if there was something that had no limits to what you could put into it ?

Last but certainly not least... How accessible is my money in this IRA

Just like with your 401k if you take any money out of this account before you're 59 1/2 then you'll have to pay a 10% penalty ON-TOP of the withdrawal being taxed as ordinary income

Now there are a few more exceptions to this rule when it comes to your IRA

Penalty Exceptions

The IRS allows several exceptions to the 10% early withdrawal penalty (though regular income tax may still apply to traditional IRA withdrawals):

Unreimbursed Medical Expenses: If they exceed 7.5% of your adjusted gross income (AGI).

Health Insurance Premiums: If you are unemployed and have received unemployment compensation for 12 consecutive weeks.

Qualified Higher Education Expenses: For you, your spouse, children, or grandchildren.

First-Time Home Purchase: Up to a $10,000 lifetime limit for qualified acquisition costs.

Disability: If you become totally and permanently disabled.

Birth or Adoption Expenses: Up to $5,000 per child (each spouse can take this distribution from their own IRA).

Death: Distributions to beneficiaries after the IRA owner's death.

Substantially Equal Periodic Payments (SEPPs): A series of payments based on your life expectancy.

IRS Levy: To satisfy an IRS tax levy on the account.

Qualified Military Reservist Distributions: If called to active duty for at least 180 days.

Emergency Personal Expense: One distribution per calendar year up to $1,000 for an unforeseeable or immediate financial need (distributions after December 31, 2023).

There are multiple IRA accounts aside from the Traditional IRA

Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred. Withdrawals in retirement are taxed as ordinary income.

Roth IRA: Contributions are made with after-tax money, so they are not tax-deductible. Qualified withdrawals and earnings in retirement are tax-free.

Rollover IRA : An account set up to receive funds rolled over from a previous employer's retirement plan, such as a 401(k).

SEP IRA : Designed for self-employed people and small business owners to save for themselves and their employees. Contributions are tax-deductible and grow tax-deferred.

SIMPLE IRA : Available to small businesses that don't have another retirement plan. Both employers and employees can contribute, similar to a 401(k) but with simpler administration.

Spousal IRA : Allows a spouse with no or little income to contribute to their own IRA, based on the working spouse's income.

Roth Conversion IRA : An account that holds funds converted from a traditional IRA to a Roth IRA. You pay taxes on the converted amount in the year of conversion.

While the rules stay consistent for most of these accounts there are some inconsistencies. If you'd like to learn more follow this link to the IRS.GOV website to dive deeper.

Want a RECAP? Check out this video

What if there was an account where you could put in as much as you want every year.. the withdrawals were completely tax free... AND you could access the money in the account WHENEVER you want with no age limitations or special circumstances ???

Well there is.. Click Below to Learn More

Follow us on Social

Get updates on new ventures through Social Media

Contact

info@leveraged-financial.com

(518) 480-8848

© 2026. All rights reserved.